BizSpace Portal

BizSpace Portal SMART Credit Business Portal

SMART Credit Business Portal Payroll Portal

Payroll Portal Supply Chain Financing

Supply Chain Financing HP Dealer Portal

HP Dealer PortalApproach and Governance

ဆုံးရှုံးနိုင်ခြေအပေါ်ခံယူချက်

ရိုးမဘဏ်၏ Risk Philosophy (ဆုံးရှုံးနိုင်ခြေအပေါ်ခံယူချက်) သည် ကျင့်ဝတ်မှန်ကန် ရိုးမဘဏ် “The Responsible Bank” ဟူသောဆောင်ပုဒ်ကို အခြေခံ၍ လိုက်နာဆောင်ရွက်လျက် ရှိပါသည်။ရိုးမဘဏ်သည် နိုင်ငံ၏ စီးပွားရေးကဏ္ဍများ ဖွံ့ဖြိုးတိုးတက်စေရန် ရည်ရွယ်ထားသည့် ဈေးကွက်များအတွင်း ငွေကြေးဝန်ဆောင်မှုများအား တိုးချဲ့ခြင်း၊ စီးပွားရေးအခွင့်အလမ်းများအား တိုးပွားအောင် ဆောင်ရွက်ကာ ဆုံးရှုံးနိုင်ခြေများကို ချိန်ဆ၍ ရေရှည်တည်တံ့သော အမြတ်အစွန်းများကို ရရှိနိုင်ရန် စွမ်းစွမ်းတမံ ဆောင်ရွက်လျက် ရှိပါသည်။

ဆုံးရှုံးနိုင်ခြေများကို အုပ်ချုပ်မှုစနစ်

ကျွန်ုပ်တို့၏ ဘုတ်အဖွဲ့သည် Yoma Bank ၏ လုပ်ဆောင်ချက်များဖြစ်သည့်

- ရိုးမဘဏ်၏ မဟာဗျူဟာဆိုင်ရာရည်ရွယ်ချက်များနှင့် ကိုက်ညီမှု ရှိစေရန်

- အရေးပါသော ဆုံးရှုံးနိုင်ခြေများကို ဖော်ထုတ်ခြင်း၊ အကဲဖြတ်ခြင်း၊ လျှော့ချခြင်းစသည့် ထိန်းချုပ်မှုများ အခြေခံမူဘောင် တို့နှင့်ထိရောက်စွာ ဆောင်ရွက်လျက်ရှိပြီး

- ဘဏ်၏ Risk appetite (လက်ခံနိုင်သော ဆုံးရှုံးနိုင်ခြေဘောင်)အတွင်းတွင် လည်ပတ်နေမှု ရှိစေရန် စသည်တို့ကို ဘုတ်အဖွဲ့၏ အဓိကလုပ်ငန်းစဥ် ဖြစ်သည့်အတွက် အထူးကြီးကြပ်စောင့်ကြည့်လျက်ရှိပါသည်။

ကော်မတီလေးခု၏ အထောက်အပံ့ဖြင့် ဘုတ်အဖွဲ့သည် ဆုံးရှုံးနိုင်ခြေများ စီမံခန့်ခွဲမှုဆိုင်ရာ မူဘောင်များ၊ ထိန်းချုပ်မှုများ (Internal Control) ကို အကျိုးသက်ရောက်မှု ရှိစေပါသည်။

- Risk Oversight Committee သည် ဆုံးရှုံးနိုင်ခြေများဆိုင်ရာ မူဝါဒများ ချမှတ်ခြင်းနှင့် လက်တွေ့အကောင်ထည်ဖော်ရန် စောင့်ကြည့်ကွပ်ကဲသည်။ ကော်မတီသည် ၎င်း၏လက်အောက်ရှိ ကော်မတီခွဲများဖြစ်သည့် အလုပ်အမှုဆောင်ချေးငွေ ကော်မတီ၊ ပေးရန်တာဝန်နှင့် ရပိုင်ခွင့်များ စီမံခန့်ခွဲရေးကော်မတီနှင့် ထုတ်ကုန်ကော်မတီတို့ကို လုပ်ငန်းတာဝန်များ ခွဲခြားပေးသည်။

- Audit Committee သည် ဘဏ်အတွင်းထိန်းချုပ်မှုများ (internal controls) ဆောင်ရွက်ပြီး၊ စာရင်းစစ်၏ လုပ်ငန်းဆောင်ရွက်မှုဆိုင်ရာ အကျိုးသက်ရောက်မှု ရှိ၊ မရှိ ကို စစ်ဆေးသည်။

- People, Remuneration and Nomination Advisory Committee သည် ဘဏ်၏ ဝန်ထမ်းများနှင့် လုပ်ခလစာဆိုင်ရာ မဟာဗျူဟာများ၊ မူဝါဒများ၊ မူဘောင်များနှင့် အလေ့အကျင့်များကို သင့်လျော်သော ကြီးကြပ်ကွပ်ကဲမှုနှင့် လမ်းညွှန်မှုများကို သေချာစေပါသည်။

- Technology Adviosry Committee သည် ဘဏ်၏ နည်းပညာ မဟာဗျူဟာနှင့် ထိုသို့သော မဟာဗျူဟာကို ပံ့ပိုးရာတွင် သိသာထင်ရှားသော ရင်းနှီးမြှုပ်နှံမှုများ၊ ဘဏ်၏ နည်းပညာပိုင်းဆိုင်ရာ ဆုံးရှုံးနိုင်ခြေစီမံခန့်ခွဲမှု၊ လုံခြုံရေးမူဘောင်နှင့် ၎င်း၏ အကျိုးသက်ရောက်မှုတို့အတွက်လည်း Risk Oversight Committee နှင့် ပူးပေါင်းဆောင်ရွက်ကာ ကြီးကြပ်ကွပ်ကဲသည်။

အမှုဆောင်အရာရှိချုပ် နှင့် ဆုံးရှုံးနိုင်ခြေများစီမံခန့်ခွဲရေးဆိုင်ရာအရာရှိချုပ် တို့သည် ဒါရိုက်တာအဖွဲ့နှင့် ဆုံးရှုံးနိုင်ခြေ စီမံခန့်ခွဲမှု ကော်မတီတို့ အတည်ပြုထားသော ဘဏ်၏ဆုံးရှုံးနိုင်သော အန္တရာယ်များနှင့် ပတ်သက်သည့် မူဝါဒများနှင့် လမ်းစဉ်များကို အကောင်အထည်ဖော် ဆောင်ရွက်ရန် တာဝန်ယူပါသည်။

အလုပ်အမှုဆောင် ချေးငွေကော်မတီ

အလုပ်အမှုဆောင်ချေးငွေကော်မတီ (ECC) သည် ဘဏ်၏ ချေးငွေဆိုင်ရာဆုံးရှုံးနိုင်ခြေမူဝါဒနှင့် လမ်းညွှန်ချက်များ၊ လုပ်ထုံးလုပ်နည်းများကို အကောင်အထည် ဖော်ဆောင်သည့်အပြင် ၎င်းတို့ကို စီးပွားရေးလုပ်ငန်းယူနစ်အားလုံးတွင် တစ်သမတ်တည်း လိုက်နာကျင့်သုံးစေရမည်ဖြစ်သည်။ ထို့အပြင် ချေးငွေဆုံးရှုံးနိုင်ခြေမူဘောင် ကန့်သတ်ချက်များနှင့် ဥပဒေရေးရာကိစ္စများအပါအဝင် လုပ်ထုံးလုပ်နည်း ဆိုင်ရာ လိုအပ်ချက်များနှင့် ချေးငွေနှင့်သက်ဆိုင်သည့် ဘဏ်အတွင်းချမှတ်ထားသော မူဝါဒများနှင့် ကိုက်ညီစေရန် သေချာစွာ လုပ်ဆောင်ရမည် ဖြစ်သည်။

အလုပ်အမှုဆောင်ချေးငွေကော်မတီ (ECC) ၏ လုပ်ငန်းဆောင်တာများတွင် – ချေးငွေဆိုင်ရာ မဟာဗျူဟာ ကို ပြန်လည်သုံးသပ်ခြင်း၊ ချေးငွေ အချက်အလက် အရည်အသွေး အလားအလာများ နှင့် ပေါ်ပေါက် လာနိုင်သော ချေးငွေဆိုင်ရာ ဆုံးရှုံးနိုင်ခြေများကို သုံးသပ်ခြင်း၊ ပြောင်းလဲနေသော မဟာဗျူဟာနှင့် ပြင်ပပတ်ဝန်းကျင် အခြေအနေများနှင့်အညီ asset writing မဟာဗျူဟာများ တိုးတက်အောင်ပြုလုပ်ခြင်း နှင့် ချေးငွေထုတ်ကုန်များနှင့် အစီအစဉ်များကို Risk Oversight Committee သို့ မတင်ပြမီ ပြန်လည်စိစစ် သုံးသပ်ခြင်းတို့ ပါဝင်သည်။

ပေးရန်တာဝန်နှင့် ရပိုင်ခွင့်များ စီမံခန့်ခွဲရေးကော်မတီ

ပေးရန်တာဝန်နှင့် ရပိုင်ခွင့်များ စီမံခန့်ခွဲရေးကော်မတီ၏ လုပ်ပိုင်ခွင့်မှာ Asset-Liability Management (ALM) မူဝါဒကို အကောင်အထည်ဖော်ရန်နှင့် ၎င်းတွင် ဖော်ပြထားသော ဆုံးရှုံးနိုင်ခြေ အန္တရာယ်များကို ကြီးကြပ်ရန်ဖြစ်သည်။ ALM သည် ဖော်ပြပါ အဓိကလုပ်ဆောင်ချက်များနှင့် ဆုံးရှုံးနိုင်ခြေများ အကျုံးဝင်ပါသည်။ အရင်းအနှီးလုံလောက်မှု၊ ငွေဖြစ်လွယ်မှု၊ အတိုးနှုန်းအန္တရာယ်၊ နိုင်ငံခြားငွေလဲလှယ်မှု၊ အခြားစျေးကွက် ဆုံးရှုံးနိုင်ခြေများကို ဖော်ပြသည်။ ALCO သည် အဓိက မဟာဗျူဟာကျသော အခန်းကဏ္ဍဖြစ်သော ဘဏ်၏ လက်ကျန်ငွေစာရင်း၏ ဖွဲ့စည်းပုံကို စီမံခန့်ခွဲခြင်း၊ ဘဏ်လုပ်ငန်း ထုတ်ကုန်အားလုံးအတွက်စျေးနှုန်းသတ်မှတ်ခြင်း နှင့် စီးပွားရေးအရ ဖွံ့ဖြိုးတိုးတက်မှု အစီအစဉ်များကို ထောက်ပံ့ရန်ငွေကြေး လုံလောက်မှုရှိခြင်းနှင့် ဘဏ်ရှိ အခြားဆက်စပ်သော တာဝန်ဝတ္တရားများနှင့်ဥပဒေအရ ချမှတ်ထားသော သက်ဆိုင်ရာ စည်းမျဉ်းများ ပါဝင်သည်။

ရရန်မသေချာသော ချေးငွေ (NPL)

ထုတ်ကုန်ကော်မတီ

ထုတ်ကုန် ကော်မတီ၏လုပ်ပိုင်ခွင့်မှာ ပစ္စည်းနှင့် ဝန်ဆောင်မှုအသစ်များ ထုတ်လုပ်ရာတွင် ထုတ်ကုန်၏ မူဝါဒ၊ လက်ခံနိုင်သော ဆုံးရှုံးနိုင်ခြေနှင့် ဈေးကွက်၏ ဝယ်လိုအားနှင့်အညီ ထုတ်လုပ်စေနိုင်ရန်ဖြစ်သည်။ ကော်မတီသည် ထုတ်ကုန်၏ လုပ်ဆောင်ချက်ကို ပြန်လည်ဆန်းစစ်ရုံသာမက လက်ရှိ ထုတ်ကုန်များအတွက် လိုအပ်သော ပြုပြင်မွမ်းမံခြင်းများကိုလည်းပြန်လည် ထည့်သွင်းစဉ်းစားပါသည်။

အကျပ်အတည်း စီမံခန့်ခွဲရေးအဖွဲ့

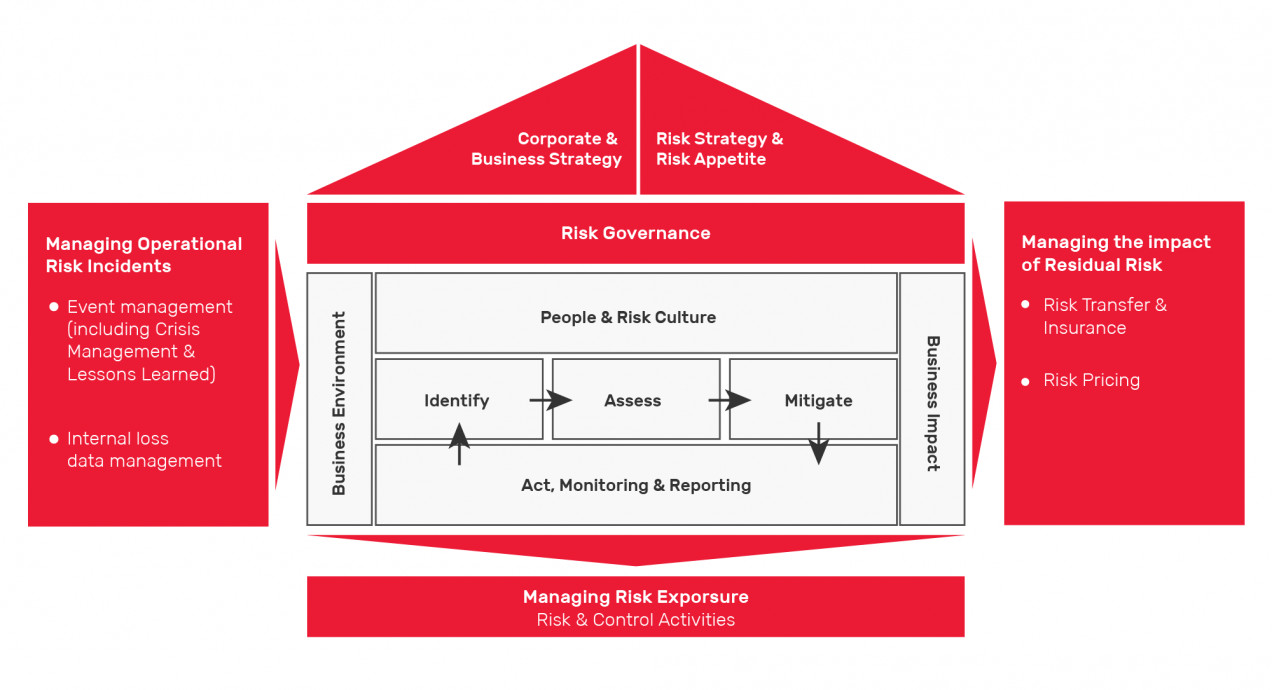

ဆုံးရှုံးနိုင်ခြေ စီမံခန့်ခွဲရေး မူဘောင်

- ရိုးမဘဏ်တွင် ကျွန်ုပ်တို့၏ Customer များ၊ ဝန်ထမ်းများနှင့်ဘဏ်ကို ကာကွယ်ရန်အတွက် Customer များအား အသိပညာပေးခြင်း၊ ဝန်ထမ်းများအား အသိပညာပေးခြင်းနှင့်လုပ်ဆောင်ချက်ပိုင်းဆိုင်ရာ လိုအပ်ချက်များကို မြှင့်တင်ပေးခြင်းတို့ကို ဦးစားပေးလုပ်ဆောင်သည့် ငွေရေးကြေးရေးဆိုင်ရာ လိမ်လည်မှု တားဆီးကာကွယ်ရေးနှင့် လျော့ချနိုင်ရေး အစီအစဉ်တစ်ရပ် ရှိပါသည်။ ရိုးမဘဏ်တွင် Customer များ၏ တိုင်ကြားချက်များကို စောင့်ကြည့်၊ မှတ်တမ်းတင်ရန်နှင့် ဖြေရှင်းရန် သီးသန့် Customer Care Centre နှင့် ဆိုရှယ်မီဒီယာလူမှုဆက်ဆံရေးအဖွဲ့တို့နှင့် ဆုံးရှုံးနိုင်ခြေ ဖြစ်ရပ်များကို စီမံခန့်ခွဲသည့်မူ ဘောင် တစ်ခု ကို လည်း ထားရှိထားပါသည်။

- လုပ်ငန်းစဉ်ဆက်မပြတ် စီမံခန့်ခွဲမှုသည် ကျွန်ုပ်တို့၏ Customer များအတွက် ထုတ်ကုန်များ နှင့် ဝန်ဆောင်မှုများကို စဉ်ဆက်မပြတ်ပေး နိုင်ရန်အတွက် အရေးပါသော အခန်းကဏ္ဍ မှ ပါဝင်လျက်ရှိပါသည်။ လုပ်ငန်းစဉ်ဆက်မပြတ် စီမံခန့်ခွဲမှု ၏ တစ်စိတ်တစ်ပိုင်းအနေဖြင့် ရိုးမဘဏ်သည် ဝန်ဆောင်မှုများအတွက် ကြီးမားသော အနှောင့်အယှက်များ မရှိစေရေးအတွက် အကျပ်အတည်းစီမံခန့်ခွဲရေး အဖွဲ့ (Crisis Management Team) ကို ဖွဲ့စည်းထားခြင်း၊ ဘေးအန္တရာယ် ပြန်လည်ထူထောင်ရေး နည်းပညာဆိုင်ရာ အခြေခံအဆောက်အအုံများ မြှင့်တင်ပေးခြင်း၊ အရေးပေါ် လေ့ကျင့်မှုနှင့် tabletop လေ့ကျင့်ခန်းများ ဆောင်ရွက်ခြင်း၊ သင်တန်းများ ပြုလုပ်ခြင်း အစရှိသည့် လုပ်ငန်းစဉ် ဆက်မပြတ်စီမံခန့်ခွဲမှုဆိုင်ရာ လုပ်ဆောင်နိုင်ရေးများကို ဆောင်ရွက်လျက်ရှိပါသည်။

- ယခုဘဏ္ဍနှစ် အတွင်းတွင် ကနဦး သဘာဝပတ်ဝန်းကျင် နှင့် လူမှုရေးဆိုင်ရာ ဆုံးရှုံးနိုင်ခြေများ အကဲဖြတ်ခြင်း လုပ်ငန်းစဉ်ကို ဆောင်ရွက်ထား ရှိပြီးဖြစ်ပါသည်။ ထို အကဲဖြတ်ခြင်း လုပ်ငန်းစဉ်သည် ရိုးမဘဏ်၏ ဆုံးရှုံးနိုင်ခြေကာကွယ်ပေးသော ပထမလိုင်းရှိ ဘဏ်ဝန်ဆောင်မှု ပေးသည့်အဖွဲ့များကို ၎င်းတို့နှင့် သက်ဆိုင်သည့် ချေးငွေကိစ္စရပ်များတွင် သဘာဝပတ်ဝန်းကျင် နှင့် လူမှုရေးဆိုင်ရာ ဆုံးရှုံးနိုင်ခြေများကို ဖော်ထုတ်ရာ၌ အထောက်အပံ့ပေးလျက်ရှိပါသည်။ ထို့အပြင် ၎င်းအကဲဖြတ်ခြင်း လုပ်ငန်းစဉ်သည် သဘာဝပတ်ဝန်းကျင်နှင့် လူမှုရေးဆိုင်ရာ ဆုံးရှုံးနိုင်ခြေများကို အကဲဖြတ်ခြင်း လုပ်ငန်းစဉ်၌သာမက ရိုးမဘဏ်၏ သဘာဝပတ်ဝန်းကျင် နှင့် လူမှုရေးမူဝါဒအပေါ် လိုက်နာဆောင်ရွက်မှုကို မြှင့်တင်ပေးပါသည်။

လက်ခံနိုင်သော ဆုံးရှုံးနိုင်ခြေမူဘောင် လုပ်ငန်းစဉ်

Three Lines of Defence Model

| First Line of Defence Risk Management | Second Line of Defence Risk Oversight | Third Line of Defence Independent Assurance |

| – Takes and manage risk exposure in accordance with the risk appetite, mandate and limits set by the Board | – Ensures key risks are escalated to Board and provides oversight to ensure First Line business executed in line with the bank’s risk appetite | – Provides the Board with an independent opinion about the effectiveness of Risk Management and Internal Controls |

| – Identifies and escalates significant emerging issues related to risk | – Develops the Risk Management Framework (policies, systems, processes, tools) | – Confirms the level of compliance with regulations, and other limits and requirements as defined in the Bank’s policies |

ဆက်စပ် အကြောင်းအရာများ

အဓိကကျသော ဆုံးရှုံးနိုင်ခြေများ

ဘဏ်မှချေးငွေ ချေးယူသူမှ ဘဏ္ဍာရေးပိုင်းဆိုင်ရာ စည်းမျည်းစည်းကမ်:များ နှင့် တာဝန်ဝတ္တရားများအား ဆောင်ရွက်ရန်ပျက်ပြားခြင်းမှ ဖြစ်ပေါ်လာနိုင်သော ဆုံးရှုံးနိုင်ခြေများ ကိုဆိုလိုပါသည်။

Read More